In this week’s big picture series we discuss how current central bank signalling is impacting global asset classes and the macro-economy as a whole.

Global equity markets rallied firmly this week with the S&P 500, Japan’s Nikkei and the UK FTSE all trading to new fiscal year highs. Global Fixed Income rallied as well with long-term yields pushing lower across the developed market spectrum as the Fed continued to signal their “intention” to lower interest rates despite inflation rates continuing to trend above target. Even countries where tighter monetary policy is warranted, such as Japan, central Banks are ensuring that they remain firmly more “dovish” than market expectations. These dovish tendencies are fuelling global asset markets, pushing down on global bond yields and creating demand for hard assets.

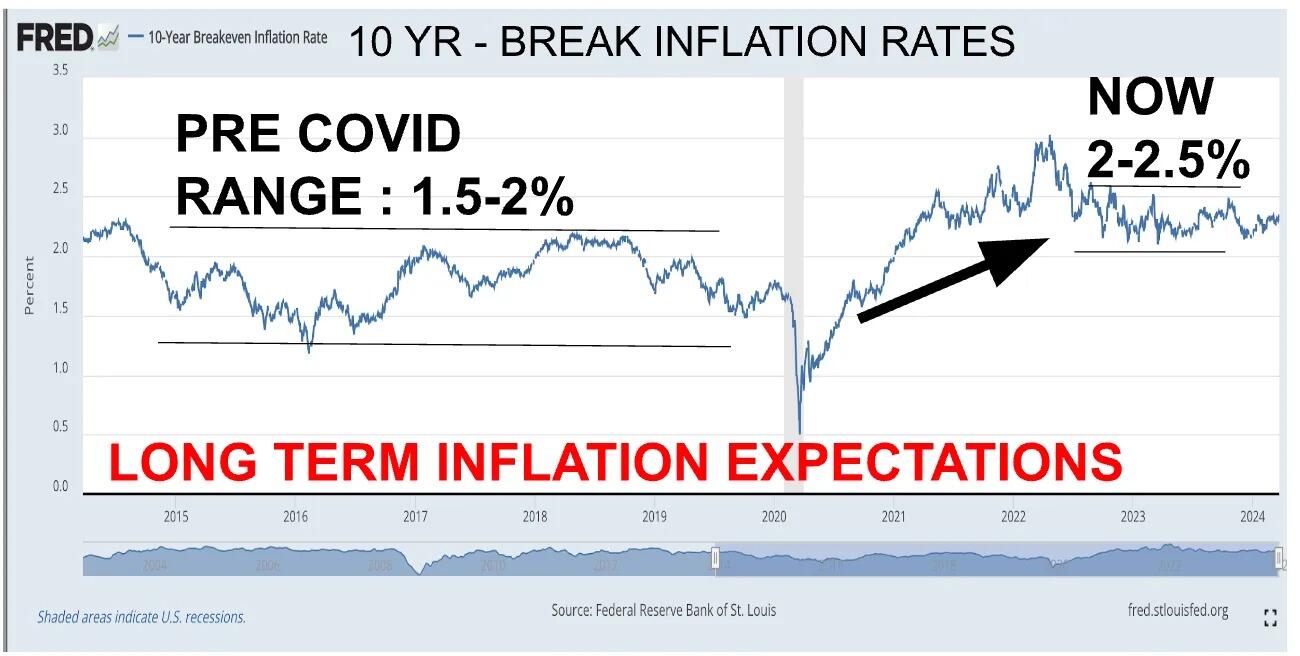

Long-term breakeven rates are heading up, oil inventories remain tight and demand for residential real estate seems to be picking as evidenced by last weeks data on US existing home sales which jumped 9.5% for the month of February, a one year high.

Over in China, stimulus measures are starting to feed into real economic activity with both Industrial Production and Fixed Asset Investment numbers coming in stronger than expectations at 7% and 4.2% respectively.

The Fed’s Chairman, Jay Powell, was notably dovish on Thursday despite revising up forecasts for GDP and Inflation. Over in Japan, the BOJ continued to push ahead with QE despite marginally raising its overnight rate at Monday’s meeting and the Bank of England implied a dovish tilt when it met on Wednesday. The net affect as mentioned earlier has been a powerful asset market rally and now rising inflation expectations.

Central Banks by signalling to markets that they “intend” to reduce policy rates at some point in the future have in reality already started doing so. Paradoxically, the longer they maintain that posture the longer it may take to bring global inflation rates back to below target as lower rates fuel economic activity and underpin inflationary pressures. Intentions are a powerful thing.

We are set to receive PCE data out of the US on Friday with markets forecasting a 0.4% increase on the headline number. US Pending and New Home sales data are also set to be released following the strong existing home sales number we received last week.

We shall also keep a close eye on oil inventories, due to be released on Wednesday, following ongoing evidence that conditions remain somewhat tight.

It is a unique moment in the global macro economy. Inflationary pressures are apparent, asset markets are explosive yet central banks are choosing to be more dovish than what would otherwise be warranted. Time of course will reveal whether macro conditions move towards the Fed’s predictions or the Fed re-calibrates in light of macro conditions.