Commercial real estate is beginning to roll over – and last week, we saw the alarming domino effect on regional banks.

Regular Digest readers know that for months, we’ve been running a “commercial real estate watch” segment to monitor this critically important sector of the U.S. economy.

The core problem reduces to elevated refinancing costs (based on the Fed’s rate hikes) that are inflicting serious pain on the commercial real estate sector.

As commercial real estate loans are now coming due at a time when property values and rental incomes have been slashed, defaults are in the cards, and the $20-trillion commercial real estate sector is wobbling.

If defaults snowball, it will have an enormous impact on the U.S. economy, specifically, the regional banking sector. That’s because regional banks account for a whopping 67% of all commercial real estate lending (they also comprise about 38% of all outstanding loans, regardless of sector).

This brings us to last week, when two key banks fired warning shots over the commercial real estate/regional banking sectors

From Bloomberg:

The US commercial real estate market has been in turmoil since the onset of the Covid-19 pandemic. But New York Community Bancorp and Japan’s Aozora Bank Ltd. delivered a reminder that some lenders are only just beginning to feel the pain.

New York Community Bancorp’s decisions to slash its dividend and stockpile reserves sent its stock down a record 38% on Wednesday, with the fallout dragging the shares to a 23-year low on Thursday.

The selling bled overnight into Europe and Asia, where Tokyo-based Aozora plunged more than 20% after warning of US commercial-property losses and Frankfurt’s Deutsche Bank AG more than quadrupled its US real estate loss provisions.

The commercial real estate sector needs lower interest rates immediately – and not just by a quarter point or so

It needs Federal Reserve Chairman Jerome Powell to take a hacksaw to the Fed Funds Rate.

That’s not going to happen. Last Friday’s blazing-hot jobs report shows the Fed won’t be cutting rates anytime soon.

Over the weekend, I read a handful of analysts now suggesting the first-rate cut won’t come until November.

And why should it? The economy is roaring. If anything, it needs a cold shower.

But without rate cuts in the near future, get ready for a double whammy: first, for commercial real estate; second, for Wall Street when it throws a tantrum because it hasn’t gotten its way with rate cuts.

As recently as December 27th, Wall Street put 90% odds on the first rate-cut coming in March. Well, Powell crushed those hopes last Wednesday in his post-FOMC press conference when he all-but-said there won’t be cuts in March.

On Sunday, Powell reiterated that during an interview on 60 Minutes.

Meanwhile, about one month ago, Wall Street was pricing in the equivalent of six quarter-point interest rate cuts by December 2024.

Even if the Fed begins cutting in April, six cuts feels aggressive and unlikely. And that means Wall Street has some repricing to do, and commercial real estate shouldn’t expect relief anytime soon.

Make sure you’re comfortable with portfolio’s exposure to commercial real estate and regional banks. There’s more pain coming.

Meanwhile, keep your eyes on institutional investors

Institutional investors are not perfect. Like regular investors, they pick plenty of duds, as well as choose the wrong times to buy and sell stocks.

That said, institutional investors are typically seen as more informed than the average investor. So, we shouldn’t ignore what they’re doing.

And what, exactly, is that?

Selling U.S. stocks.

From biedexmarkets.com:

The recent trading week saw a notable shift with institutional clients engaging in significant selling, marking the first outflow from single stocks in eight weeks, according to Bank of America’s analysis of client data…

This wave of selling was primarily led by institutional clients, who recorded their second-largest outflow since 2008, and the largest since 2015, with a focus on selling Tech and Discretionary stocks.

Source: BofA Securities

So, where is this money going? And do you want to follow it with some of your own capital?

We’re seeing flows pick up toward emerging market (EM) stocks.

Though the U.S. market has dominated returns over EM stocks for a decade, that could be changing.

From Reuters:

Inflows into emerging markets remained strong, BofA added, with a $6.8 billion inflow to stocks in the week to Wednesday…

China alone saw a $6.3 billion inflow into stocks, following on from an almost $12 billion inflow the previous week. This meant the past four weeks saw the largest cumulative inflow on record of just over $21 billion…

BofA added that its Bull & Bear Indicator rose to a 2-1/2 year high of 6.1 from 6.0, helped by very strong inflows into emerging market stocks.

To be clear, this is not a suggestion to bail on your U.S. holdings and go big into EM. But history shows that a portfolio with geographic diversity is a great way to reduce overall volatility and drawdowns.

On top of that, some EM markets are offering far more attractive valuations than U.S. stocks. So, moving some money into EM isn’t purely defensive – there’s an offensive firepower aspect too.

Remember, as the Fed begins cutting rates, it will weaken the dollar which helps EM stocks. Couple that with lower valuations, and EM could be setting up for a solid bull run.

One way to measure the attractiveness of EM valuations is by looking CAPE ratios

“CAPE” stands for “cyclically adjust price-to-earnings” ratio. It’s the traditional PE ratio, but it uses 10 years’ worth of earnings data to smooth out business cycle fluctuations.

Today, the U.S. has a nosebleed CAPE ratio of 31.

Compare that to China at 9.6, Hong Kong at 11.4, or Brazil at 12.2.

But watch out for India. At 36.5, its CAPE is even higher than that of the U.S.

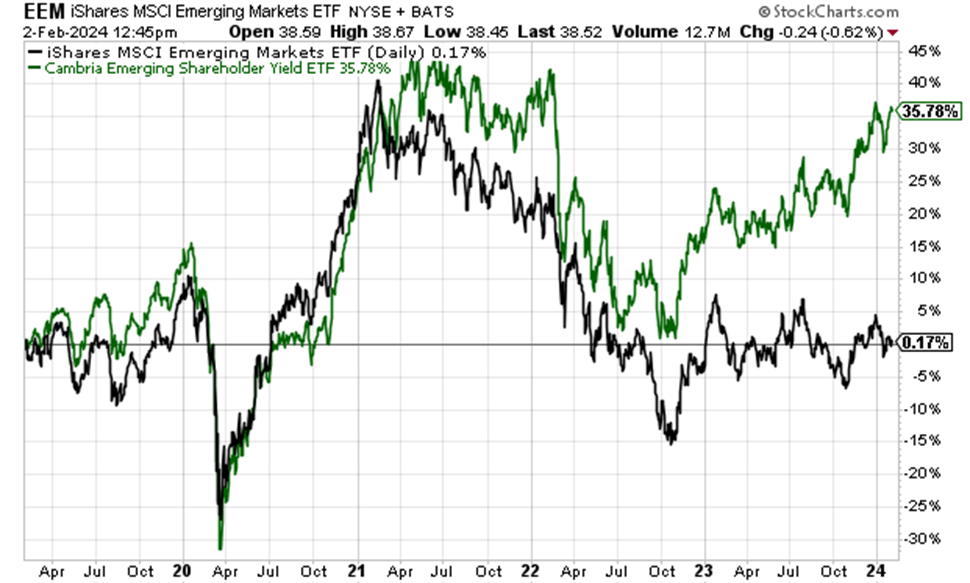

If you’re interested in emerging market stocks, check out EEM, which is the iShares MSCI Emerging Markets ETF. Also, look at EYLD, which is the Cambria Emerging Shareholder Yield ETF.

Full disclosure, I’m a personal friend of Cambria’s CEO Meb Faber. But the chart below that compares EEM (in black) to EYLD (in green) over the last five years shows why you might want to consider EYLD if you’re interested in emerging markets today.

Source: StockCharts.com

Moving around the world, keep your eyes on the Red Sea

Over the weekend, the United States carried out retaliatory strikes against Iran-backed groups in Iraq and Syria.

To make sure we’re all on the same page, repeated attacks by Houthi militants on commercial ships in the Red Sea have impacted trade routes, shipping times, and global supply chains.

So far, western governments haven’t been successful in stopping these Houthi attacks. This has led to warnings of impending costs that will hit consumers here at home.

From CNBC:

The world’s largest shipping company, MSC, and several retail and trade experts warned Congress on Tuesday that if the Red Sea chaos caused by Houthi rebel attacks is not stopped, the rise in freight prices will spread further into the global economy and hit consumer wallets…

Maritime advisory firm Sea-Intelligence said the average delay for late vessel arrivals has “deteriorated,” increasing by 0.30 days month over month to 5.35 days…

National Retail Federation companies are seeing container prices double from $1,500- $3,000, Jon Gold, its vice president of supply chain and customs policy, told the House subcommittee.

“This represents a 38%-73% cost increase for directly affected cargo,” Gold said. “We are seeing some costs being passed onto the consumer now from the smaller and medium businesses.”

On Friday, President Biden authorized attacks that hit a series of Mideast targets.

From NBC:

The dozens of airstrikes launched by the United States late Friday are by far its biggest attacks against Iran-backed militants in the Middle East during this current round of conflict.

However, the strikes in Iraq and Syria, an initial retaliation for the killing of three American soldiers, did not go as far as some more hawkish figures had hoped, as the White House tries to avoid an all-out war with Iran.

It’s too early to determine the effectiveness of these strikes on the Houthi stranglehold on the Red Sea. But we need it to be effective. Otherwise, consider the big-picture ramifications…

What does Wall Street want? Rate cuts.

What is the Fed watching that will influence the timing and scope of those rate cuts? Inflation.

What variable can push inflation the wrong direction this spring? Increased consumer prices due to longer shipping routes to avoid the Red Sea.

It’s just another reminder why we should be cautious about how Wall Street has been pricing stocks.

Finally, if you live in New York, I’m sorry…

While not an investing story, this is a sign of the times.

Inflation is still impacting everyone, everywhere. Manhattan is no exception.

New York’s “congestion pricing” plan for Midtown Manhattan, scheduled to begin later this year, is going to make it that much harder for regular families to make ends meet.

From The Wall Street Journal:

If [the Metropolitan Transportation Authority] has its way, drivers entering Manhattan south of 60th Street will pay a daily driving tax of $15—nearly $4,000 a year—if they have an E-ZPass account. Those without one will be billed $22.50 a day by mail.

New York being New York, it doesn’t stop there.

The MTA has unilateral authority to declare “Gridlock Alert Days” whenever it needs to line its pockets more, which will add 25% surge pricing to the daily invoice. The state has also reserved the authority to raise the congestion tax by 10% in 2024, its very first year.

For drivers entering the city from New Jersey and suburban Rockland County, N.Y., the congestion tax is a looming nightmare. Drivers will pay as much as $24.75 a day on top of the $17-a-day bridge and tunnel tolls, plus the cost of gasoline and parking.

A single trip into the city could easily cost families $100 before they even get a cup of coffee or a bite to eat.

Ah, New York.

Perhaps it’s time to change the slogan from “the city that never sleeps” to “the city that never sleeps on a chance to fleece you.”

Have a good evening,

Jeff Remsburg