- The USD Index (DXY) extended its range bound theme around 104.00.

- Fed’s rate cut bets continued to lean towards a June move.

- Markets now shift their attention to NFP and Powell’s testimonies.

- Fed officials maintained the hawkish tilt throughout the week.

The Greenback navigated the week with a slight upside bias, regaining the 104.00 hurdle and beyond when tracked by the USD Index (DXY) and managing to close the week with decent gains after the previous pullback.

The index, in the meantime, managed well to keep its business just above the critical 200-day SMA (103.74), always against the backdrop of the equally side-lined fashion US yields across different time frames.

Meanwhile, investors’ speculations remained firm around the likelihood that the Federal Reserve (Fed) might kick off its easing cycle at the June 12 gathering, or even later in light of the strong resilience of the US economy, sticky (albeit in a downward path) inflation and the still tight labour market.

Underpinning the above, the FedWatch Tool measured by CME Group maintains the probability of a reduction of the Fed Funds Target Range (FFTR) by 25 bps in June at nearly 52%, up from around 5% a month ago.

The increasing likelihood of a “soft landing” for the US economy allowed Fed policymakers to maintain a hawkish-ish tone in their comments, leaving the door open to a June, and even later-than-June rate cut.

That said, Atlanta Fed President Raphael Bostic suggested this week that it might be suitable to lower the policy rate during the summer, mentioning that economic indicators will determine the timing of rate cuts. His comments fell in line with his colleague Austan Goolsbee from the Chicago Fed, who expressed his disagreement with the notion of waiting until core inflation reaches 2% on a 12-month basis before considering rate cuts, advocating instead for rate adjustments to be linked to confidence in progress toward the target rate. However, Richmond Fed Thomas Barkin said on Friday that he is in no rush to cut rates, even hinting at the idea that the Fed might not reduce its rates at all this year.

The latter appears somewhat propped up after US inflation figures measured by the Personal Consumption Expenditures (PCE) rose more than estimated during January, adding to previous readings in the same line from the Consumer Price Index (CPI) and Producer Prices (PPI).

Regarding central banks and the inflationary process within the G10 sphere, a comparison can be drawn between the Fed and its significant counterparts (excluding the Bank of Japan). This comparison underscores that both the European Central Bank (ECB) and the Bank of England (BoE) are expected to postpone policy rate reductions until after the summer.

US fundamentals continue to point to a healthy economy

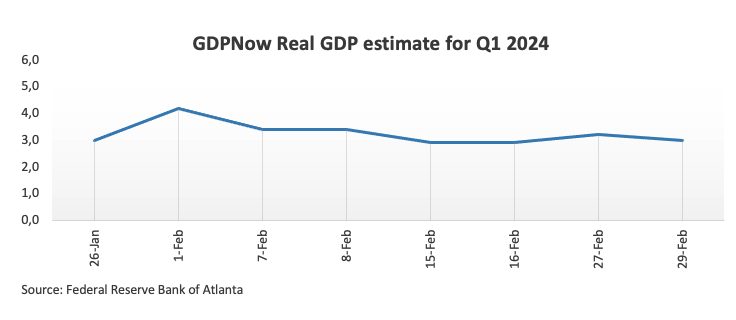

Unlike previous weeks, this time the data releases came in on a more moderated fashion, as Durable Goods Orders missed consensus in January (-6.1% MoM), the Consumer Confidence gauged by the Conference Board surprised to the downside in February (106.7), weekly Initial Jobless Claims increased a tad higher than estimates and another revision of the GDP Growth Rate showed the economy expanded 3.2% YoY during the October-December period. Despite this week’s weakness in the calendar, fundamentals remain well on the strong side and keep underpinning the prospect of a “soft landing”.

DXY technical outlook

On the daily chart, the 2024 highs for DXY, which are located around 105.00 (February 14), represent the first area of resistance. After this area is passed, a small obstacle lies ahead at the weekly peak of 106.00 (November 10) seconded by the November top of 107.11 (November 1).

The immediate conflict zone, however, lines up at the 200-day SMA of 103.74 if sellers get control. This is ahead of the short-term 55-day SMA at 103.19 and the weekly low of 102.77, which was reached on January 24. If the DXY declines further, it may reach its December low of 100.61 (December 28), which is before the critical 100.00 barrier and the 2023 low of 99.57 printed on July 14.

Furthermore, while above the 200-day SMA, the outlook for the index is expected to remain constructive.